The Hidden Pitfalls of the “Under ¥200,000 in Miscellaneous Income” Rule— You Thought You Didn’t Need to File, But Maybe You Actually Do —

“You don’t need to file a tax return if your side income is under ¥200,000.”

Many people have probably heard this before.

In fact, for salaried employees, miscellaneous income from side jobs totaling ¥200,000 or less per year is generally exempt from filing a final tax return.

However, there are quite a few cases where people later realize:

“I thought I was safe because it was under ¥200,000, but it turned out I actually needed to file.”

Today, let’s summarise some commonly overlooked points regarding miscellaneous income.

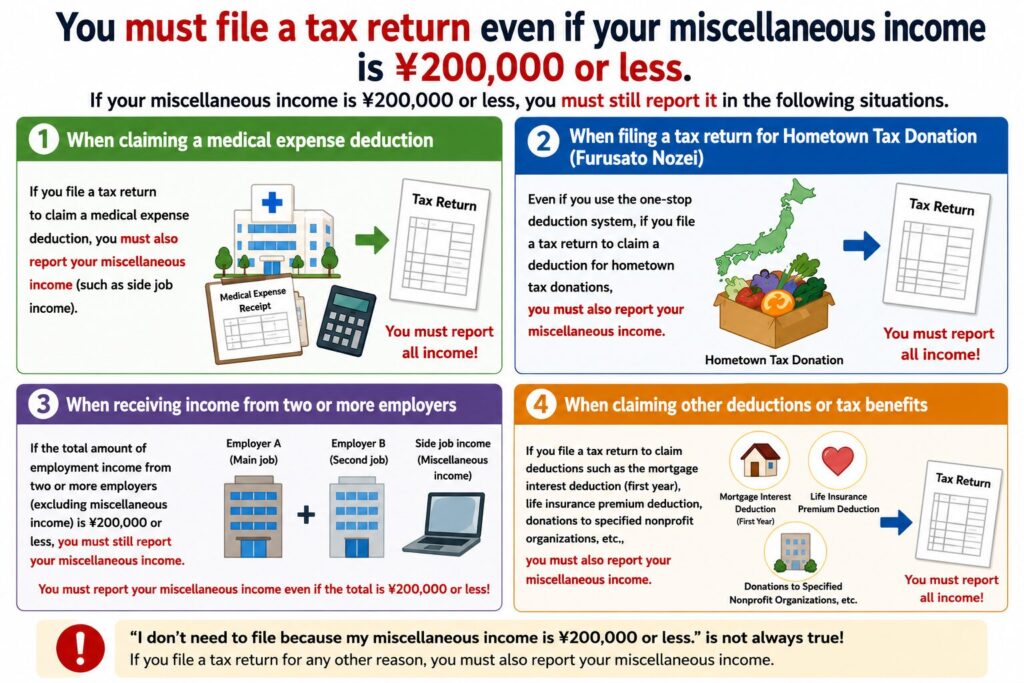

The “Under ¥200,000 Means No Filing Required” Rule Is Not Absolute

This rule actually comes with certain conditions.

For example, if you are filing a tax return for other reasons, such as:

- claiming medical expense deductions,

- filing due to hometown tax donations (furusato nozei),

- receiving salary income from two or more employers,

then the special exemption for “miscellaneous income under ¥200,000” no longer applies.

In other words, situations like the following can occur:

“I filed a tax return to claim medical expense deductions, and then realized I also had to report my side income.”

Miscellaneous Income Can Include Unexpected Items

When people hear “miscellaneous income,” many think only of side-job earnings.

But in reality, it may also include things such as:

- pensions,

- manuscript fees,

- speaking fees,

- foreign currency deposit exchange gains,

among others.

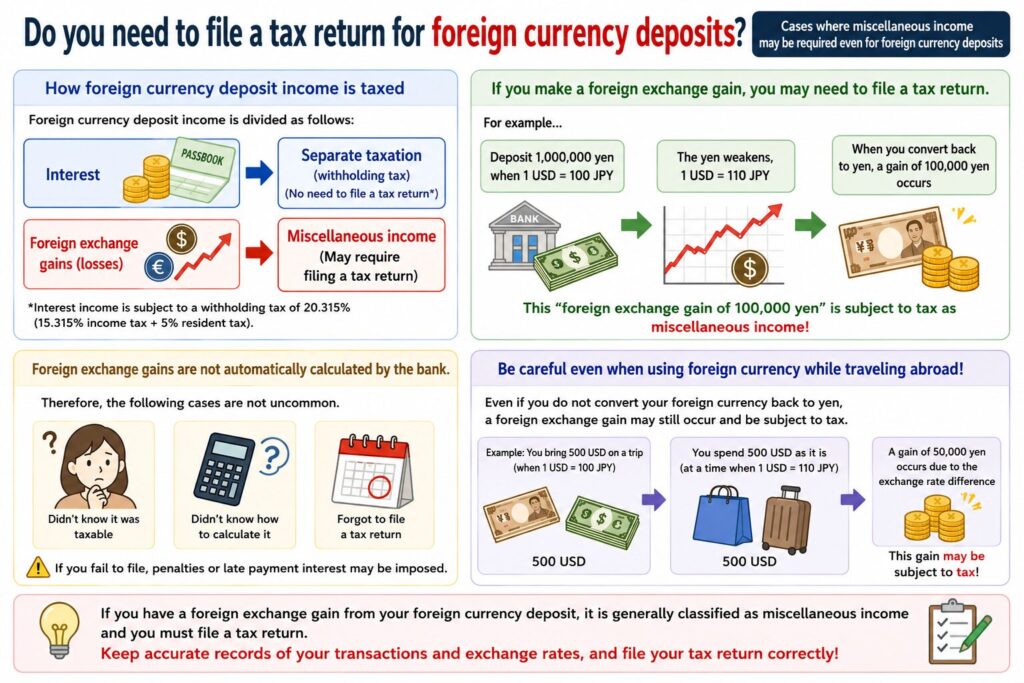

One area that deserves particular attention is foreign currency deposit exchange gains.

Do Foreign Currency Deposits Also Require Tax Filing?

With foreign currency deposits:

- Interest income → taxed separately at source

- Foreign exchange gains → treated as miscellaneous income

This means that if you earn profits due to currency fluctuations, you may need to file a tax return.

What makes this even trickier is that these exchange gains are not automatically calculated by banks.

As a result, many people end up in situations such as:

- not realizing the gains were taxable,

- not knowing how to calculate them,

- forgetting to report them.

Furthermore, even if you simply used foreign currency for overseas travel expenses, exchange gains may still be considered taxable under certain circumstances.

Looking Only at “How Much Your Assets Increased” Can Be Misleading

When building assets, people naturally tend to focus on:

“How much can my money grow?”

However, the actual amount you keep can be affected by factors such as:

- taxes,

- tax filing obligations,

- fees,

- regulatory rules.

Especially with products like foreign currency deposits, there are cases where:

“I thought I had made a profit, but then realized tax procedures were required.”

The Important Thing Is Understanding the Rules

Tax systems are complicated, but not knowing the rules does not exempt you from them.

That’s why it’s important to understand in advance:

- what category your income falls under,

- whether filing is required,

- how taxes are applied.

When managing assets, it may be important to consider not only “returns,” but also the tax system surrounding them.

\ Get the latest news /