Should You Buy Bond Funds in NISA? The 2026 Reform and the “All Country + Government Bonds” Approach

In this article, I would like to discuss a topic that has recently regained attention among investors: the relationship between NISA and bonds.

Many investors may be asking themselves:

- Should I simply invest in the All Country Index Fund (eMAXIS Slim All Country) or the S&P 500 through NISA?

- Is the traditional “4-Asset Balanced Portfolio” still a valid investment strategy today?

As we enter an era in which interest rates are gradually returning, it may be time to rethink how we construct our investment portfolios.

NISA Alone Cannot Complete Your Asset Allocation

NISA (Nippon Individual Savings Account) is an excellent tax-advantaged investment program that allows investment gains to grow tax-free.

In recent years, many investors have started building wealth through low-cost index funds such as global equity funds and S&P 500 funds.

However, NISA has one notable limitation:

It does not allow investors to hold true safe assets such as cash deposits or Japanese government savings bonds.

Assets Eligible for NISA

- Stocks

- Investment trusts (mutual funds)

- ETFs

- REITs

- Bond funds

- Certain public bond investment trusts (scheduled to become eligible in 2026)

Assets Not Eligible for NISA

- Ordinary bank deposits

- Time deposits

- Japanese Government Savings Bonds for Individuals

- Cash

As a result, investors who rely solely on NISA may end up holding only assets whose values fluctuate in the market.

For this reason, it may be helpful to think in terms of:

- Holding risk assets within NISA

- Holding safe assets outside NISA

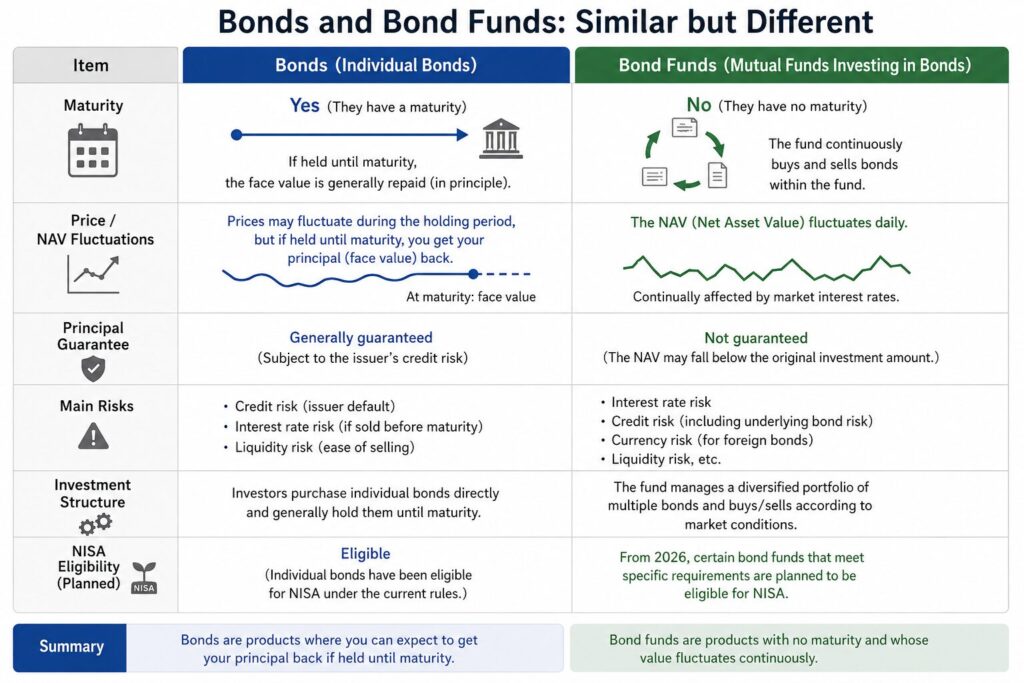

Bonds and Bond Funds Are Not the Same Thing

Beginning in 2026, certain public bond investment trusts are expected to become eligible investments under NISA.

Before discussing this change, it is important to understand the difference between directly owning bonds and investing in bond funds.

Direct Bond Ownership

With highly creditworthy bonds, such as government bonds, temporary market price fluctuations generally do not matter if the bond is held until maturity.

The key feature is that bonds have a maturity date.

Bond Funds

Bond funds, on the other hand, do not have a maturity date.

Fund managers continuously buy and sell bonds, meaning the fund remains exposed to changing interest rates at all times.

As a result, the fund’s net asset value fluctuates daily, and principal is not guaranteed.

Bond Funds Are Vulnerable to Rising Interest Rates

Bond prices and market interest rates generally move in opposite directions.

- When interest rates fall, bond prices rise.

- When interest rates rise, bond prices fall.

From the late 1990s through around 2020, interest rates generally declined, providing a favorable environment for bond funds.

However, since 2022, global interest rates have risen significantly, causing many bond funds to decline in value.

Although bond funds are typically less volatile than stocks, they should not be mistaken for principal-protected safe assets.

Is It Time to Reconsider the Traditional 4-Asset Portfolio?

For many years, a common investment strategy in Japan was the so-called “4-Asset Balanced Portfolio,” which allocates assets equally among:

- Japanese equities

- International equities

- Japanese bonds

- International bonds

Each asset class represents 25% of the portfolio.

Meanwhile, the late economic commentator and investment expert Hajime Yamasaki advocated a much simpler approach:

- A global stock index fund (All Country)

- Japanese Government Savings Bonds for Individuals (10-year variable-rate)

His philosophy was straightforward:

Allow global equities to drive long-term growth while using government bonds as the truly defensive portion of the portfolio.

At the same time, Japan’s public pension fund, Government Pension Investment Fund (GPIF), continues to use a diversified four-asset allocation strategy.

This does not mean that the 4-asset approach is wrong. However, GPIF is a massive institutional investor responsible for preserving pension assets, and its investment objectives differ significantly from those of individual investors.

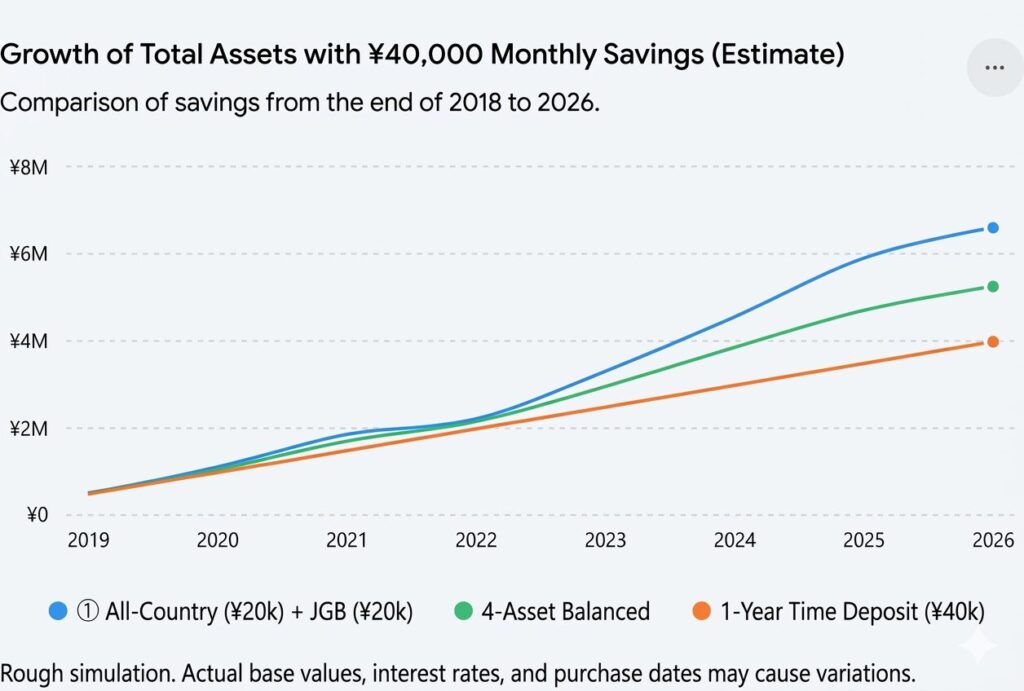

A Simple Simulation

The following example assumes monthly investments beginning in 2018 and continuing through 2026.

Past performance does not guarantee future results.

| Strategy | Total Contributions | Approximate Portfolio Value |

|---|---|---|

| All Country Fund + Government Bonds (¥20,000 each per month) | ~¥3.8 million | ~¥6.6 million |

| 4-Asset Balanced Portfolio (¥10,000 in each asset class per month) | ~¥3.8 million | ~¥5.25 million |

| Time Deposit (¥40,000 per month) | ~¥3.8 million | ~¥3.98 million |

Within this specific period, the simple combination of a global equity fund and government bonds produced the strongest result.

Of course, future outcomes may differ.

The most important question is not which product wins, but whether you can maintain your chosen asset allocation with confidence over the long term.

This simulation is a rough illustration created using ChatGPT and historical market data. It is intended for educational purposes only and does not guarantee actual investment results.

A Portfolio Strategy for the Future

Successful investing requires clearly separating the role of growth from the role of protection.

Growth Assets (The Accelerator)

- All Country global equity funds

- Global stock index funds

These assets seek to capture long-term global economic growth.

Defensive Assets (The Brake)

- Japanese Government Savings Bonds for Individuals (10-year variable-rate)

- Time deposits

- Cash reserves

These assets help stabilize the overall portfolio.

The key is determining the appropriate balance between growth and safety based on your personal risk tolerance.

Conclusion

Starting in 2026, public bond investment trusts will become available within NISA, expanding investors’ options.

However, a newly eligible product is not necessarily the best choice.

NISA is an excellent tool for growing wealth, but it is not designed to hold truly safe assets.

That is why it may be useful to think about portfolio construction as:

- Holding growth assets inside NISA

- Holding safe assets outside NISA

As interest rates return after many years of ultra-low-rate policies, now may be a good time to review your own portfolio and reconsider not only how to grow your assets, but also how to protect them.

\ Get the latest news /