In an Era of Ultra-Low Interest Rates, Are Assets Really Losing Value?

“You can’t grow your money just by leaving it in the bank.”

“With ultra-low interest rates, cash keeps losing its value.”

We hear these kinds of comments more and more often today.

It is true that ordinary savings accounts in today’s ultra-low interest rate environment offer interest rates of only around 0.001% per year.

As a result, many people feel anxious that “keeping money in savings alone may gradually reduce the value of their assets.”

But is that really the case?

In this article, we would like to examine the relationship between ultra-low interest rates and inflation from a slightly different perspective.

The “100-Year Time Deposit” of the Meiji Era

In 1900 (Meiji 33), a Japanese bank introduced a financial product called the “100-Year Time Deposit.”

The idea was simple: deposit 1 yen for 100 years, and it would grow to 10,000 yen at maturity.

This corresponded to an annual interest rate of approximately 9.75% — an extraordinarily high rate by today’s standards.

However, when the deposit matured in the year 2000, the holder received exactly what had been promised on paper: 10,000 yen.

What makes this story particularly interesting is the value of “1 yen” during the Meiji era.

It is often said that 1 yen at that time would be worth roughly 5,000 yen in today’s terms.

Based on that calculation, 10,000 yen in the Meiji era could be considered equivalent to roughly 50 million yen today.

Yet the actual 10,000 yen received at maturity clearly did not possess that level of purchasing power.

In other words, even though the deposit grew enormously in nominal terms over 100 years, once inflation is taken into account, the real value of the money may not have increased nearly as dramatically as the numbers suggest.

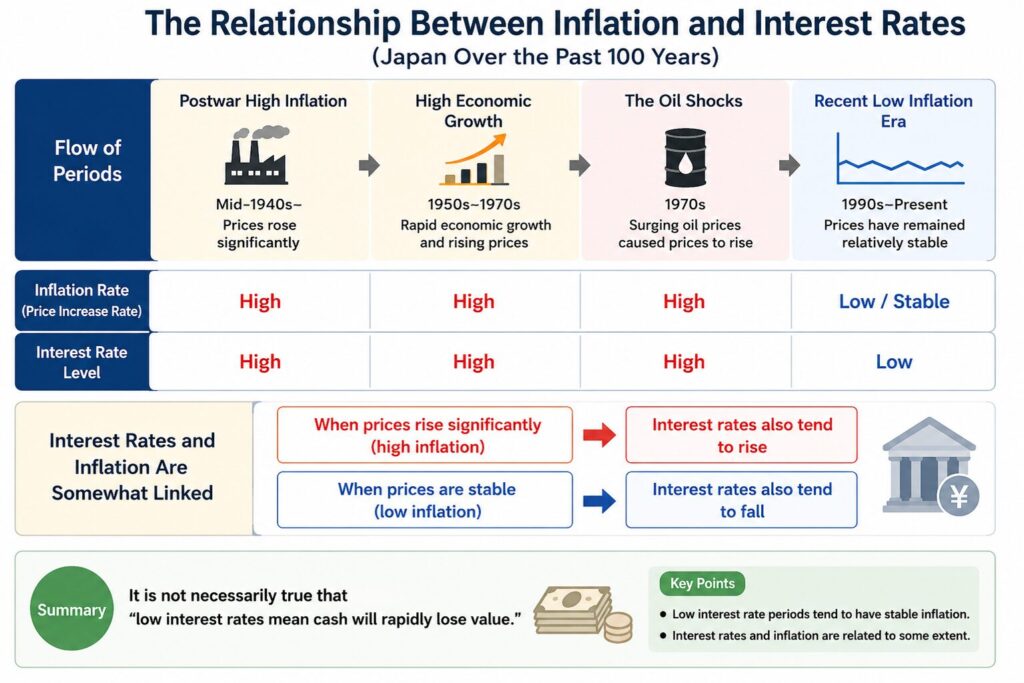

The Relationship Between Inflation and Interest Rates

Over the past century, Japan experienced periods of significant inflation, including:

- Rapid postwar inflation

- The era of high economic growth

- The oil shocks of the 1970s

In other words, the high interest rates of the past existed alongside substantial inflation.

By contrast, recent ultra-low interest rate environment is also characterized by relatively modest inflation.

This suggests that interest rates and inflation are linked to some extent.

When prices rise sharply, interest rates also tend to rise.

When prices remain stable, interest rates generally stay low.

For that reason, it may be too simplistic to conclude that:

“Low interest rates automatically mean that cash rapidly loses value.”

One Yen in the Meiji Era and 10,000 Yen Today

The difference in value between 1 yen in the Meiji era and 10,000 yen today may not be as large as people commonly imagine.

That said, they are certainly not exactly equal in value.

Moreover, it was not only prices that changed over the past century.

Society itself has changed dramatically in terms of:

- Income levels

- Working conditions

- Infrastructure

- Consumer lifestyles

- Social security systems

As a result, simply converting historical currency values into modern equivalents does not necessarily capture the true meaning of “wealth” or quality of life.

Perhaps the more important point is not that:

“High interest rates dramatically increased asset values,”

but rather that:

“High inflation was one reason interest rates were high.”

From that perspective, the gap between 1 yen in the Meiji era and 10,000 yen today may not be as extreme as the numbers alone imply.

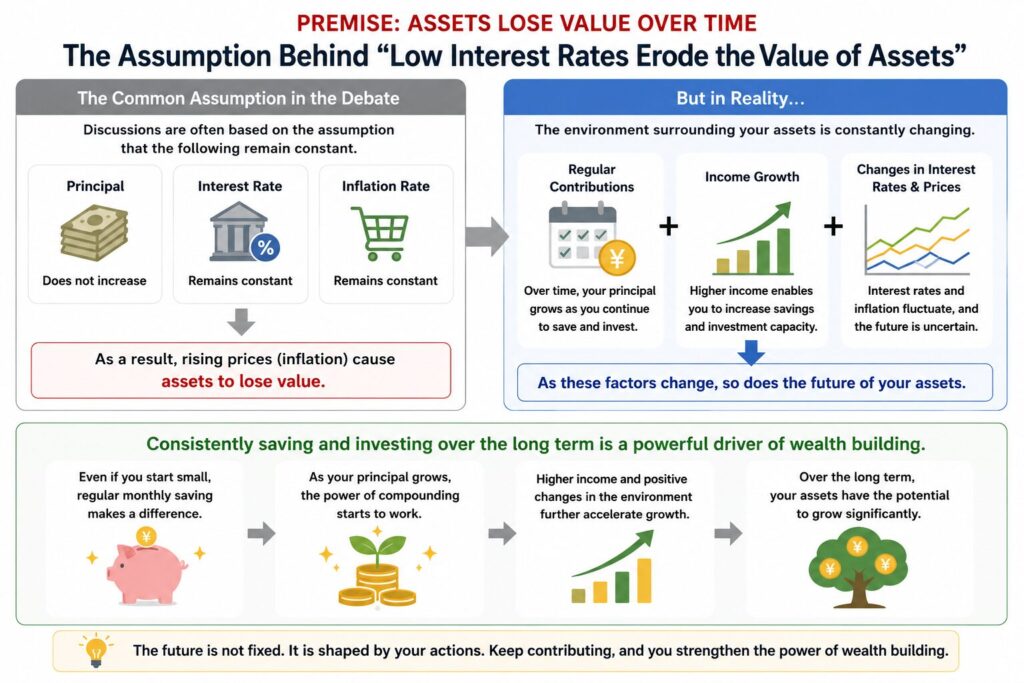

The Assumption That “Assets Lose Value”

Arguments that “low interest rates cause assets to lose value” often rely on several assumptions:

- Principal never increases

- Interest rates remain fixed

- Inflation remains constant

In reality, however, financial conditions are constantly changing due to factors such as:

- Monthly savings contributions

- Rising income

- Changes in interest rates and prices

Steadily saving money over long periods of time has itself been an important force in building assets.

Conclusion

It is certainly true that money is harder to grow in an era of ultra-low interest rates.

At the same time, however:

- Inflation has remained relatively moderate

- Interest rates and inflation tend to move together

- Regular savings contributions gradually increase principal

Considering these factors, it may be overly simplistic to conclude that “keeping money only in savings inevitably leads to a continuous loss of asset value.”

When thinking about long-term asset formation, it may be more important not to focus solely on interest rates, but also to consider:

- Inflation

- Income levels

- Living standards

- Ongoing savings contributions

from a broader, long-term perspective.

\ Get the latest news /