What Is the Gift Tax Settlement System Upon Inheritance? -Understanding the Benefits and Risks in Light of Recent Tax Reforms –

In this article, we will take a closer look at Japan’s “Gift Tax Settlement System Upon Inheritance” , including the impact of recent tax reforms.

This system is often discussed as part of inheritance planning, but its rules can be complicated, and many people wonder:

- “Is it actually beneficial?”

- “How is it different from annual gifting?”

- “Is it true that once you choose it, you cannot go back?”

Recent reforms have made the system easier to use in some respects, but there are still important points to keep in mind.

So here, we will try to explain the basic structure of the system and the key points to consider as clearly and simply as possible.

The Difference Between Gift Tax and Inheritance Tax

When you transfer your assets to another person, taxes may apply.

- If the transfer is made during your lifetime, it is generally subject to gift tax.

- If the transfer occurs after death, it is generally subject to inheritance tax.

In general, gift tax rates are set higher than inheritance tax rates for the same amount of assets.

One reason is that inheritance assets are considered to have a role in supporting surviving family members, so inheritance tax is designed to impose a lighter burden in many cases.

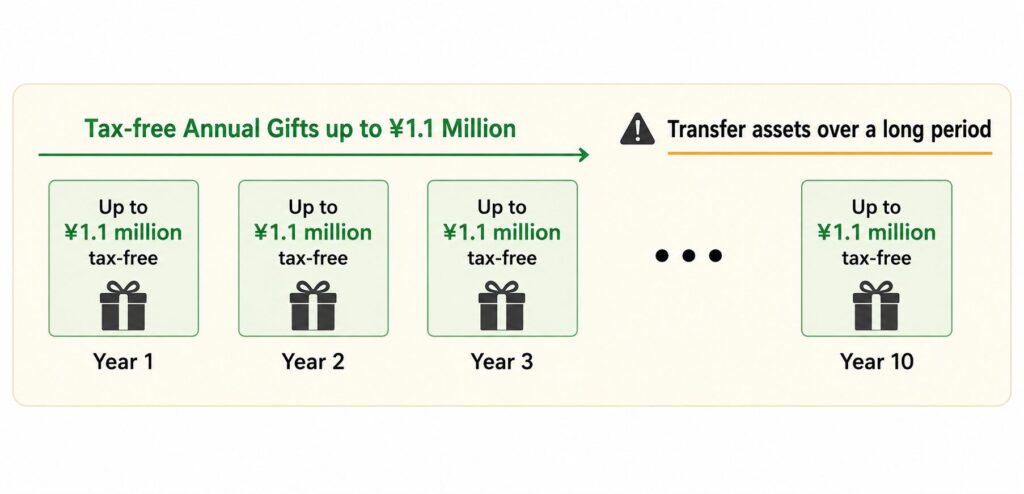

What Is Annual Gifting?

Under the ordinary gift tax system, gift tax is imposed on the amount received in a year after deducting the annual exemption of 1.1 million yen.

In other words, gifts of up to 1.1 million yen per year are generally exempt from gift tax.

Because of this, many people have used a strategy of:

“Giving 1.1 million yen each year”

to gradually transfer assets over a long period of time.

This is commonly referred to as annual gifting.

However, even if gifts are structured to appear as annual gifts, the tax authorities may deny the arrangement depending on the actual circumstances, so careful planning is necessary.

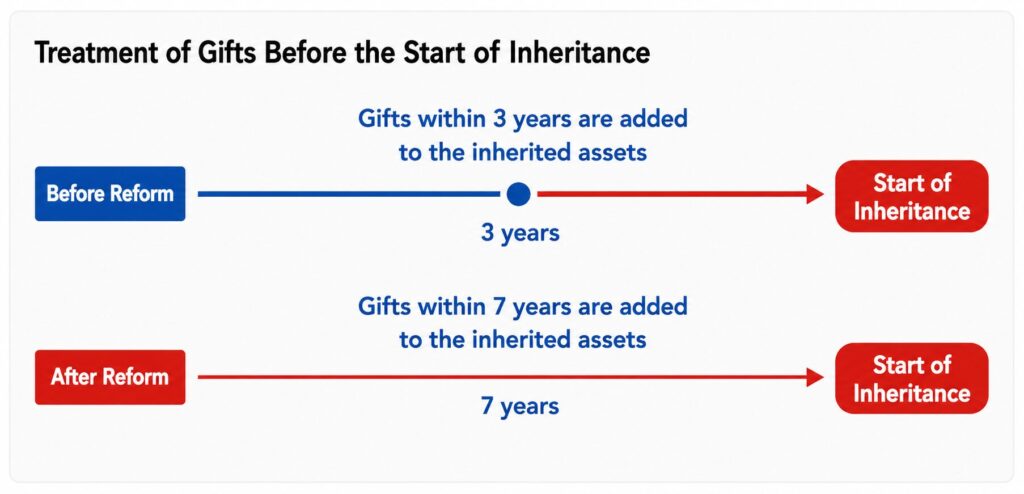

Recent Reform: The “7-Year Rule”

The annual 1.1 million yen exemption cannot necessarily be used right up until death.

Previously, gifts made within three years before death were added back when calculating inheritance tax, meaning the benefit of the annual exemption was effectively lost for those gifts.

Under recent tax reform, this period is being gradually extended from three years to seven years.

As a result, gifts made within seven years before the start of inheritance proceedings may now be included when calculating inheritance tax.

For this reason, anyone intending to use annual gifting as part of inheritance planning needs to begin planning well in advance.

Why Was the Gift Tax Settlement System Created?

Traditionally:

- Transfers during life → gift tax

- Transfers after death → inheritance tax

However, because gift tax rates were relatively high, there was concern that wealth transfers from older generations to younger generations were not progressing smoothly.

To encourage earlier transfers of wealth, the Gift Tax Settlement System Upon Inheritance was introduced.

How the System Works

Simply put, this system:

“Reduces the tax burden at the time of gifting and settles the tax later when inheritance occurs.”

The key point is:

“Assets given during life are ultimately treated as part of the inheritance tax calculation.”

Up to 25 Million Yen Can Be Gifted Without Immediate Gift Tax

Under this system:

- Cumulative gifts up to 25 million yen are exempt from gift tax

- Any amount above that is taxed at a flat 20% rate

At first glance, this may appear more favorable than ordinary gift tax rules.

However, this system assumes that the gifted assets will ultimately be taken into account at the time of inheritance.

As a result, depending on the size of the estate, it may sometimes have been more advantageous to pay ordinary gift tax at the time of the gift instead.

In addition, even in situations where inheritance tax might not normally arise, using this system could create an unexpected inheritance tax burden because past gifts are included in the calculation.

How the Final Tax Settlement Works

When inheritance occurs:

- The inheritance assets

- The assets previously gifted under this system

are combined to calculate inheritance tax.

Any gift tax already paid is then credited against the inheritance tax liability.

In other words, the system can be viewed as:

“A system that encourages transfers of assets during life while ultimately settling the taxes through inheritance tax.”

Major Changes Under the 2024 Reform

Before 2024, the system was often considered difficult to use because:

- The annual 1.1 million yen exemption was unavailable

- Once chosen, taxpayers could not return to the ordinary annual gifting system

However, major reforms were introduced in 2024.

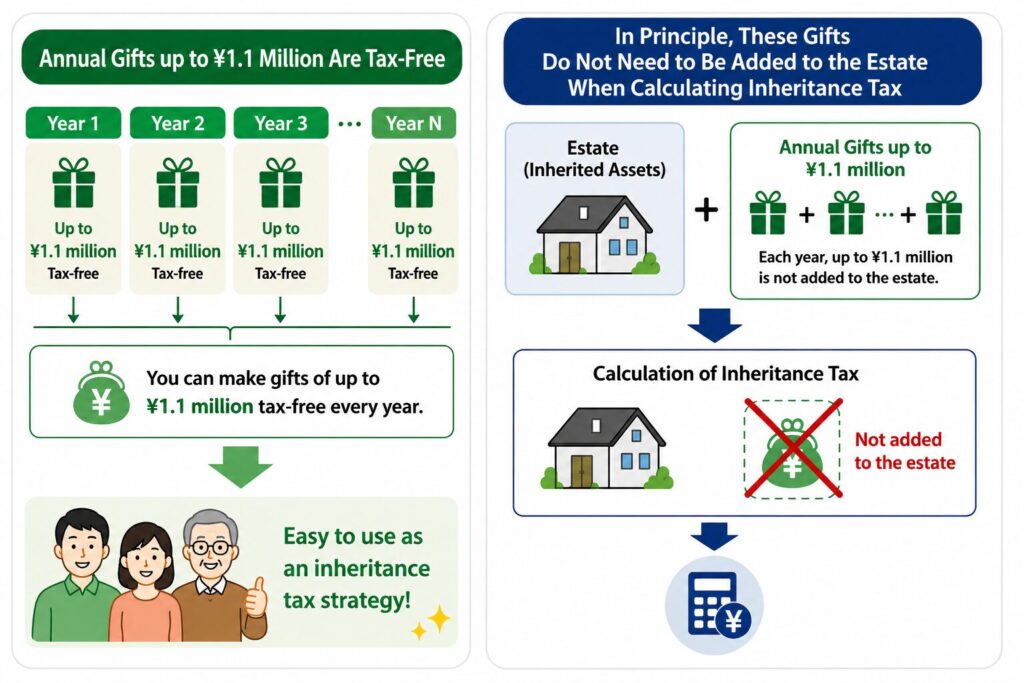

A new annual basic exemption of 1.1 million yen was added.

In principle, gifts within this annual exemption no longer need to be included in inheritance tax calculations.

In addition, this exempt portion is no longer affected by the special annual gifting restrictions that require gifts made within a certain number of years before death to be included in inheritance tax calculations.

As a result:

- Annual gifts up to 1.1 million yen are tax-free

- Those amounts generally do not need to be added back for inheritance tax purposes

This has made the system far more useful for inheritance planning.

This reform is currently attracting considerable attention in the field of estate planning.

However, these benefits are available only if the Gift Tax Settlement System Upon Inheritance is formally elected.

Important Points to Consider

Despite the advantages, there are also important risks and limitations.

The biggest point is:

“Once selected, you cannot return to the ordinary annual gifting system.”

Even if problems arise later, the election generally cannot be changed midway.

In other words, the decision may affect your tax situation for many years.

Relationship With the Statute of Limitations on Gift Tax

Another important feature of this system relates to the statute of limitations for gift tax.

Under ordinary annual gifting, gift tax is generally subject to a statute of limitations.

After six years (or seven years in cases involving serious misconduct), it becomes difficult for the tax authorities to impose additional gift tax.

Under the Gift Tax Settlement System Upon Inheritance, however, gifted assets remain part of the inheritance tax calculation until inheritance occurs.

Therefore:

- Gifts made 20 years ago

- Gifts made 30 years ago

may still be included in the inheritance tax calculation.

Under ordinary annual gifting, older gifts gradually become less likely to create tax issues over time.

Under this system, however, even very old gifts remain part of the calculation until inheritance takes place.

Future Tax Burdens Are Difficult to Predict

Another challenge is that it can be difficult to accurately predict the final tax burden because factors such as:

- The future size of the estate

- Future inheritance tax rates

- The timing of inheritance

are all uncertain.

In that sense, the system can also be viewed as:

“A system that carries an uncertain future tax burden.”

Inheritance Tax May Apply Even if the Inheritance Is Renounced

Another important point concerns renunciation of inheritance.

Under this system, gifted assets are treated as part of the inheritance tax calculation together with inheritance assets.

As a result, even if a person formally renounces inheritance, gifts received under this system may still be included in inheritance tax calculations.

This point is often difficult to understand, but it is extremely important to recognize before using the system.

A High-Risk, High-Return System

If used effectively, this system may produce significant tax-saving benefits.

In particular, the addition of the 1.1 million yen annual exemption under the 2024 reform is a major advantage.

At the same time, however, the system has features such as:

- You cannot reverse the choice once made

- Future tax burdens are difficult to predict

- Depending on future circumstances, the result may become disadvantageous

For that reason, it may be appropriate to view the system as:

“A system with both substantial benefits and substantial risks.”

Conclusion

The 2024 reforms have made the Gift Tax Settlement System Upon Inheritance considerably easier to use than before.

In particular:

- The annual 1.1 million yen exemption

- The exclusion of that amount from inheritance tax calculations

make the system especially attractive as an inheritance planning tool.

However, there are still important issues to consider carefully, including:

- The inability to reverse the election

- The fact that the final result depends heavily on future inheritance circumstances

Rather than focusing only on the immediate advantages, it is important to consider:

“Whether the system will truly be beneficial within the context of the overall future inheritance situation.”

If you are considering using this system, consulting with a tax professional such as a certified tax accountant is strongly recommended.

\ Get the latest news /