6. Designing and Practicing Asset Formation (Final Chapter)

In this series, we have approached asset formation in as simple a way as possible.

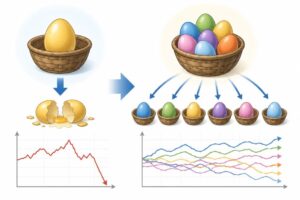

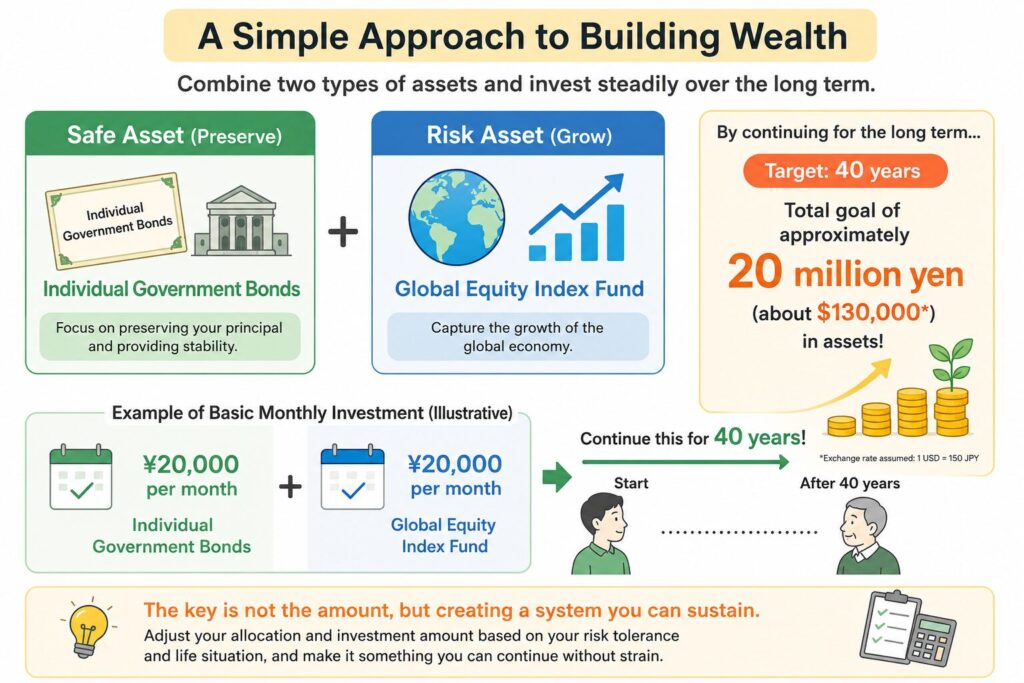

We have introduced a basic framework that combines:

- Safe assets (Japanese government bonds for individuals)

- Risk assets (global stock index investments)

The idea is to build long-term wealth by consistently investing in these two components.

A simple example of this structure is:

- Japanese government bonds: ¥20,000 per month (capital preservation)

- Global stock index: ¥20,000 per month (growth assets)

By continuing this monthly investment over a long period of 40 years, the goal is to accumulate approximately 20 million yen in total assets.

However, the allocation and investment amount will vary depending on individual risk tolerance and life circumstances.

What matters most is not the exact amount, but whether the system can be sustained without strain.

■ The Essence of Long-Term Consistency

Even if investing ¥40,000 per month is difficult, starting with ¥20,000 or even ¥10,000 is perfectly acceptable.

In long-term investing:

- The size of the amount is less important than

- The ability to continue consistently

Over time, even small investments grow steadily when supported by long periods.

Time is the most powerful factor in wealth accumulation.

■ Practical Methods for Risk Asset Investment

There are two practical ways to invest in global stock index funds as risk assets.

① Investing Through Mutual Funds

This is the simplest and most automated method.

You can invest a fixed amount every month, even with a small starting capital.

Once the system is set up, the investments continue automatically, making this approach highly suitable for building disciplined, long-term investing habits.

② Holding ETFs

If you prefer greater transparency regarding underlying holdings and pricing, Exchange-Traded Funds (ETFs) are an option.

However, ETFs generally do not support automatic fixed-amount monthly investing, so some additional steps are required:

- Using brokerage services that allow fixed-amount purchases (e.g., “kabu-kabu” type services)

- Accumulating investments through mutual funds first, then transitioning into ETFs

■ Important Considerations

When switching from mutual funds to ETFs, capital gains may be subject to taxation if profits have been realized.

Therefore, in practical terms, it is essential to utilize:

- The NISA tax-advantaged investment system

- Tax-free investment limits

Specifically, the process would be:

- Accumulate investments in mutual funds within a NISA account

- Once the investment reaches a sufficient level, transition into ETFs

By properly using these systems, investors can reduce tax burdens and build wealth more efficiently.

■ Conclusion of the Series

Asset formation does not need to be complicated.

At its core, the structure is very simple:

- Safe assets (bonds)

- Growth assets (global stock index)

By separating these two and investing consistently over the long term, a solid foundation for wealth building can be established.

■ Final Remarks

The central message of this series has been:

Not “choosing complicated financial products,” but rather

“building a simple and sustainable system that you can continue.”

The outcome of asset formation is determined not by knowledge alone, but by consistency over time.

By creating a system that fits your circumstances and allowing time to work in your favor, you adopt the most rational approach to long-term investing.

It is my hope that this series serves as a helpful foundation for thinking about long-term asset formation.

From the next installment onward, I’ll cover topics related to asset building and personal finance as individual topics rather than as a series.

\ Get the latest news /